Nordic wrote:Yeah, where the F is this deflation they keep harping about?

Gas is up, oil is up, food is up. So house prices have dropped, WHO THE FUCK CARES, they were in a goddamn bubble! Supposedly the biggest bubble in history.

And they're not gonna raise house prices by flooding the world with their shitty paper money.

None of this is making any sense whatsoever, unless their actual idea is to destroy the world economy, which is certainly what it SEEMS is their goal.

The ground buffalo I used to buy at the corner store was $5.99 a pound, it just went up to $7.99.

As one tiny tiny example of all the food I see going nothing but up in price.

The Boiling Frog: Effects of QE2 On The Bottom 80% of the U.S. Population Gonzalo Lira

Monday, November 8, 2010

An old metaphor: If you take a frog and drop it into a roiling pot of boiling water, it’ll jump right out, unscathed. But if you put that same frog in a pot of cold water, and then slowly raise the heat, that frog won’t move. It’ll stay in that pot of water, calm as can be, right up until it is boiled to death.

I’ve been arguing that the unpayable Federal government debt, coupled with irresponsible Federal Reserve policies, will inevitably lead to a hyperinflationary event and currency collapse. In order to prepare for a web seminar on hyperinflation in America, I’ve been looking at the issue of how to safeguard assets before a currency collapse, and how to identify opportunities in the midst of a hyperinflationary crisis.

But along the way—inevitably—it’s led me to consider the issue of the effects of hyperinflation on the American people. Not even hyperinflation—just regular old rising consumer prices: How will they affect the average household.

It’s disturbing.

Even if you don’t buy my hyperinflation call in the least—and a lot of very smart people don’t—the recently announced Quantitative Easing 2 policy of the Federal Reserve has had and will have a profound effect on the dollar.

And a profound effect on the American people—especially the bottom 80%.

Bernanke’s stated purpose in QE2 is to spark consumer spending, and thereby reignite the economy. To do this, Bernanke and the Fed will pump $600 billion into the Treasury bond market, in monthly $75 billion increments—at minimum. According to the Fed’s statement, if more “liquidity” is needed, then by golly, more liquidity will be pumped into the economy.

QE2 is really the official start of a race-to-the-bottom debasement of the U.S. dollar.

No one doubts this—and no one would dispute that such a currency debasement will bring about upward pressures on consumer prices across the board. Indeed, this is the explicit purpose of QE2: The Fed is trying to induce inflation, as it believes that inflation will bring about a reignition of the stagnant American economy.

A lot of commentators have been discussing what QE2 will mean for equities and the various bond markets. People are talking about the Treauries’ yield curve—but not much about what QE2 will mean for the rest of the American population: The middle class, the working poor, the poor, and even the upper-middle class.

So let’s give it a go:

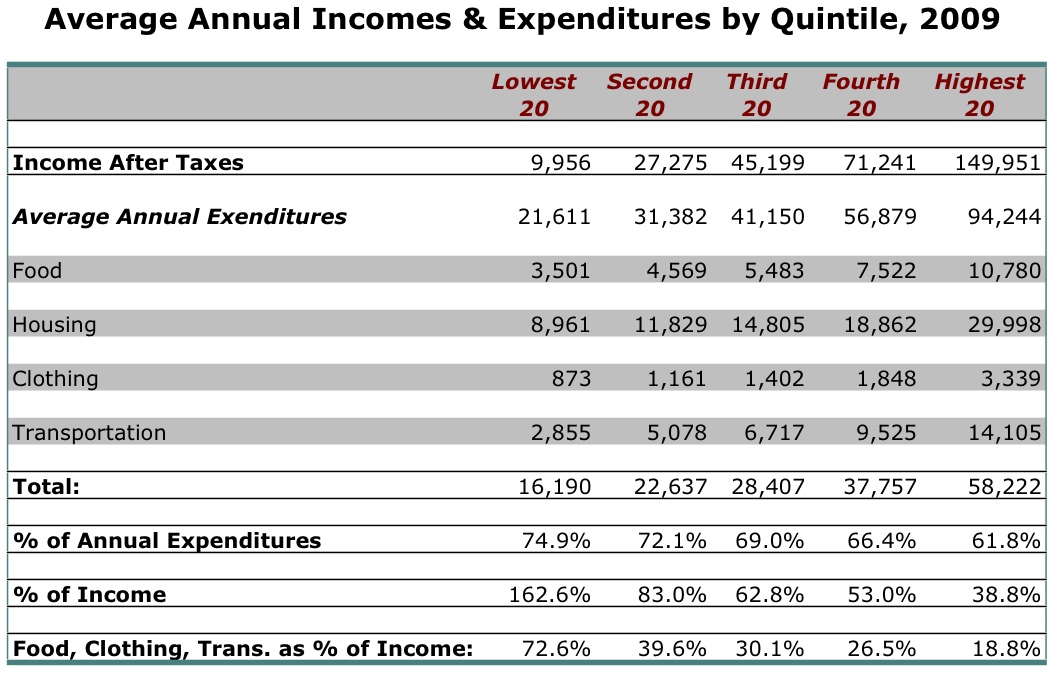

Taking Bureau of Labor Statistics data for 2009, which can be found here, we can put together this simple chart of household incomes and expenditures for last year, divided by quintiles:

Data, from Bureau of Labor Statistics, can be found here.

Data in unadjusted U.S. dollars.

(A note on the data: Housing expenditures include mortgage payments or rents, utilities, and heating, including heating oil. Transportation data includes use of public transportation. Food includes “Food Away From Home”—a remarkably high proportion of expenditures, at 41% for the entire population, skewering to almost 50% for the top quintile, and almost 30% for the lowest quintile. The figure “% of Annual Expenditures” represents how much food, housing, clothing and transportation—the basic necessities—represents of the total expenditures of each quintile. The figure “% of Income” shows the basic necessities as percentages of after-tax income for each quintile.)

Now, it’s no trick to see that rising prices of basic necessities—as a result of plain vanilla Fed-induced inflation, and not the hyperinflation I am positing—will affect everyone: But especially the middle class, the working poor and the poor.

It would be nice if we could quantify that effect. But we can’t just input a hypothetical inflation rate, apply it to the data, and come out with a number expressing how much each percentage point of inflation will affect each quintile of the population.

We can’t because, as prices rise, people buy less of a necessity: Higher gas prices means people drive less. Higher food prices means people eat less, or less quality of food. Higher heating oil prices means people heat their homes at a lower temperature—or in some cases not at all.

But although we can’t easily quantify it, we can comfortably make certain claims about the effects of rising consumer prices on the population.

The first claim I would venture to make—and one that I don’t think will be particularly controversial—is this: Any household spending more than two-thirds of their after-tax income on food, housing, clothing and transportation will suffer an immediate, negative impact from the Fed’s efforts at induced inflation.

That covers pretty much the bottom three quintiles of American households. So 60% of the U.S. population will suffer an immediate effect of rising prices—the stated policy goal of Ben Bernanke’s QE2.

QE2 is having the immediate intended effect of pushing up asset prices, bouying up the financial sector—but it’s also pushing up commodity prices, which have been rising ever since QE2 was first toyed with as a policy option back in the spring.

Lag times may vary, but rising commodity prices inevitably translate into rising consumer prices for basic necessities on Main Street.

QE2 is directly responsible for the rise in the last few weeks of all commodities. This will inevitably lead to higher consumer prices.

This inevitable effect of rising prices for the basic necessities gives lie to the stated goal that the Fed has of helping the American people by way of QE2. The policy is not helping—on the contrary:

A minimum of 60% of the population will feel immediate, unavoidable pain directly as a result of QE2. They will spend more for basic necessities than they spent previously for them.

Or else, if they don’t spend more, they will consume less. This ought to be obvious: People who cannot afford to spend more on a necessity will instead consume less of it, be it food, gas, or heating oil.

So here’s Fed Lie Number 2: QE2 will not get the economy spending again—on the contrary, rising consumer prices brought about because of QE2’s pushing up commodity prices will insure that the population cuts back on consumption, even if in nominal terms they are spending the same, or even more.

The key assumption that I am making, of course, and which has to be made in any analysis of the effects of rising consumer prices across socio-economic groups, is that wages and salaries will either not rise, or will rise with a lag time of no less than six months.

This is an easy assumption for me to make: Even in the best of economic times, wages and salaries do not rise in lockstep with an expanding economy. And we are currently not in an expanding economy.

It is reasonable to assume that, during a period of steadily rising prices coupled with stagnant economic growth, wages and salaries will not rise for at least six months, if not longer. And of course, if unemployment were to rise above the current U-6 rate of 17%, then obviously aggregate wages and salaries would contract further—which would further aggravate the effects of the rising prices of basic necessities on the bottom 60% of the population for sure. If unemployment continues to rise, then that bottom 60% would begin to grow into the bottom 70% or 80%—maybe even hit the top quintile as well.

Wages are key. If inflation hit consumer prices as well as wages in equal measure, the net effect would be zero—which is more or less what you see in ordinary expansion-driven inflation, the kind prevalent in healthy economies: There are price pressures on commodities, which eventually translate into higher prices at the supermarket—but there are also price pressures on wages, as the economy in toto is expanding, and therefore bidding up scarce labor as it grows. In an expanding economy, prices might be rising—but wages are rising too, so no complaints.

However, in a stagnating or contracting environment—such as what we are experiencing now in the American economy—there are obviously no pressures on wages: If anything, there are downward pressures on wages and salaries.

So if commodity prices rise, people—especially the poor, the working poor, and the middle-class, but maybe even the upper-middle class—are really going to take a hit, as more of their after-tax income goes to paying for basic necessities.

Some people might think that the debasing of the dollar via QE2 will mean that the real cost of housing will fall, as rents and fixed mortgages will be undermined by inflation. They might think this is a good thing.

But this only makes sense if your earnings are absolute: If you’re boss is paying you in gold coins, or silver lingots.

But if you live on a dollar income, especially a fixed income—as so many seniors do, let alone the average wage earner—even if your housing costs remain nominally static, rising food, transportation and clothing prices will still take bigger and bigger bites out of that dollar-based income. Please look at the last line of the above table—“Food, Clothing, Transportation as % of Income”—which I calculated precisely for this objection.

The only ones who won’t feel the pain of rising prices of basic necessities that bad is the top quintile—maybe. If they’re income comes predominantly from equities, maybe. If not, then they’re going to take the hit as well.

Way to go, Benny! Your QE2 is going to hit all five quintiles! Be proud!

As I have discussed in detail elsewhere, and which ought to be clear from my discussion in this post, Ben Bernanke and the fucking idiots at the Fed committed the post hoc ergo propter hoc fallacy with regards inflation: They seem to genuinely think that inflation begets growth, rather than understanding that growth begets inflation. (I don’t buy conspiracy theories that claim Benny and the Fed Fucktards are deliberately creating inflation to save the elite’s bacon—I think Benny and his Lollipop Gang are simply and genuinely stupid.) So he and his minions have started up QE2, hell bent on creating inflation in the American economy.

He seems to be succeeding, too.

According to Producer Price Index numbers, grains have risen 33% year over year, oil 20% year over year (both figures September-to-September, link is here). Ever since the idea of QE2 was floated back in May/June, commodities of all kinds have been steadily rising. And as of last week, when Quantitative Easing 2 was officially unleashed, commodity prices have surged even more—and will continue to rise for the foreseeable future. Not just precious metals but grains, sugar, coffee, not to mention oil—they are all rising.

Anecdotally, there is increasing evidence that food prices at the supermarkets have been rising for some time. I do not live in the United States, but I’m in close contact with literally dozens of people, both friends and business associates. From casual conversations and long discussions, I’ve been hearing that supermarket prices are rising across the board, and have been rising since at least mid-spring—yet the price rises do not seem to be reflected in the CPI.

That’s because of how the CPI—the Consumer Price Index, the traditional (and official) metric of U.S. inflation—is calculated. It uses data from past years—currently the 2007 and 2008 consumer survey—to create a basket of products, goods and services, which it uses to calculate monthly price changes.

However, the CPI doesn’t slice the baloney fine: If a product-x that was sold in a 20 ounce package for $3.99 back in 2007 is now being sold in an 18 oz. package at the same price, CPI does not compute that there was an 11.1% inflation in the price of product-x. Rather, according to the CPI, there was zero price inflation in product-x—because it sold for the same price, regardless of whether the package was 10% smaller.

But this is exactly what seems to be happening in food, as well as in other categories of what one would consider basic necessities: Foodstuffs are being sold in smaller units, cotton clothing is now being sold for the same price, only made of synthetic materials, and so on. A recent blog post on Zero Hedge highlighted the specific case of coffee at WalMart, previously sold in a package of 39 oz. for $9.88, now being sold for $10.48—in a 33.9 oz package. This represents a 22% jump in price. Cases such as this are common, and cropping up like mushrooms on the web—enough to confirm that stealth inflation is happening, without needing to stop by John Williams’ Shadow Government Statistics.

This brings the obvious question: If food, transportation, clothing and housing prices rise, but the CPI doesn’t measure it—was there inflation?

This isn’t a Zen koan or Berkeley’s tree falling in the woods—this is real. So my answer is obvious: Yes.

But according to the Fed and to most of the economic commentariat (except for a few notable and distinguished exceptions), since the CPI is not rising, there is no inflation. At least not in theory. In practice? That’s something else.

So! What does this all mean?

It means that Americans are the frog in the metaphor. Between 60% and 80% of them—to be precise—are slowly being boiled alive. The bottom 60% to 80%, to be even more precise.

Because of QE2 in all its iterations—its rumor back in the spring, its announcement last week, its forthcoming implementation—prices for food, housing, clothing and transportation are rising, and will continue to rise as Bernanke’s policy works its magic on commodity prices, and eventually reaches the supermarkets.

The financial sectors might be pleased that their assets are being bouyed by this flood of money coming from the Eccles Building—but the rest of the population will be drowning.

It won’t be just the bottom two-thirds of the population that will feel the pain of QE2: The upper-middle class and even the top quintile will inevitably see more and more of their income going to pay for basic necessities, while their wages and salaries remain stagnant—assuming, of course, that they’re lucky enough to still have a job.

All the while, since the Consumer Price Index will be lagging or flat, the mainstream economists and the Fed drones will keep up a steady chant of, “There is no inflation! There is no inflation!”—even as a majority of the population feels the squeeze of rising prices for the basic necessities. It’ll be a lot like a bunch of cooks, standing around the boiling pot, saying to the poor frog, “It’s only cold water! Don’t worry! It’s still cold! Trust us!”

So like the frog in the metaphor, the bottom 60% of American households will be slowly boiled alive by rising prices—

—brought by QE2.

As I said, you don’t have to buy my hyperinflation call and currency collapse scenario to realize this effect of QE2. This effect of Bernanke’s policy is immediate, undeniable, and inevitable: QE2 will hurt a vast majority of the American population, while helping only a very, very few.

To this, I say: Yeay, Benny—way to help the American people. Way to fucking go.

[

posting.php?mode=quote&f=8&p=365118 ]

"Teach them to think. Work against the government." – Wittgenstein.