The Shining The Nasdaq

Moderators: Elvis, DrVolin, Jeff

![]() by drstrangelove » Sun Jun 05, 2022 6:09 am

by drstrangelove » Sun Jun 05, 2022 6:09 am

Fitch withdraws ratings on debt-laden China Evergrande, subsidiaries

HONG KONG, June 2 (Reuters) - Fitch Ratings said on Thursday it has decided to withdraw its rating on embattled property developer China Evergrande Group (3333.HK) and two of its subsidiaries as the firms have stopped participating in the process.

The rating agency in December downgraded Evergrande and its subsidiaries, Hengda Real Estate Group Co Ltd and Tianji Holding Ltd, to so-called "restricted default" status, saying the firms had defaulted on their offshore bond obligations. read more

In its statement on Thursday, Fitch said that it would no longer have sufficient information to maintain the ratings on Evergrande, the world's most indebted developer with more than $300 billion in debt, and two of its subsidiaries.

![]() by drstrangelove » Sun Jun 12, 2022 5:39 am

by drstrangelove » Sun Jun 12, 2022 5:39 am

During the last forty-four years, my days have begun and ended with the mortgage market. Four painful moments stand out. Today makes five. (There have been many more good days, but even the Fairy Godmother has her limits.)

Mortgages are covered poorly in financial press, as stocks and such are much more entertaining. Today’s events still unfolding will take days for good coverage. Freddie’s weekly survey will not discover today until next Thursday. But the MBS market is real-time, not like old, sleepy S&L days.

The CPI news this morning was so awful that it changed the bond market’s view of Fed trajectory, and the weakest sector broke. In bond jargon, MBS went “no-bid.” No buyers for MBS. Then a few posted prices beyond borrower demand, not wanting to buy except at penalty prices. Overnight the retail consequence has been a leap from roughly 5.50% to 6.00% for low-fee 30-fixed loans.

![]() by drstrangelove » Sun Jun 12, 2022 10:47 pm

by drstrangelove » Sun Jun 12, 2022 10:47 pm

![]() by MacCruiskeen » Mon Jun 13, 2022 2:06 am

by MacCruiskeen » Mon Jun 13, 2022 2:06 am

![]() by drstrangelove » Mon Jun 13, 2022 5:35 am

by drstrangelove » Mon Jun 13, 2022 5:35 am

![]() by drstrangelove » Mon Jun 13, 2022 5:39 am

by drstrangelove » Mon Jun 13, 2022 5:39 am

![]() by Belligerent Savant » Tue Jun 14, 2022 5:41 pm

by Belligerent Savant » Tue Jun 14, 2022 5:41 pm

The Cost of Wishful Thinking on Inflation Is Going Up Too

First it wasn’t real. Then it was ‘transitory.’ Now we’re told the Fed will cure it with a few rate hikes.

By Gerard Baker

June 13, 2022 6:29 pm ET

You would think by now that, informed by so many examples from history, we would be familiar with the stages of a policy disaster in the making. Calamitous wars and foreign-policy misadventures; economic, fiscal and regulatory blunders, costly social policy initiatives—almost all seem to follow the same pattern.

First denial, the refusal to accept the mounting evidence that we are on the wrong track. Next, complacency: Even when the inconvenient facts are reluctantly acknowledged, a misplaced confidence that a small adjustment is all that is needed to snatch victory from the jaws of defeat. When that fails, the policy maker turns to wishful thinking, a doughty insistence on expecting the best in the face of the worst—everything will be all right; we have a plan premised on all the best possible assumptions. This is the terminal stage: At some point the full extent of the catastrophe is evident.

![]() by drstrangelove » Tue Jun 14, 2022 10:55 pm

by drstrangelove » Tue Jun 14, 2022 10:55 pm

The Cost of Wishful Thinking on Inflation Is Going Up Too

You would think by now that, informed by so many examples from history, we would be familiar with the stages of a policy disaster in the making. Calamitous wars and foreign-policy misadventures; economic, fiscal and regulatory blunders, costly social policy initiatives—almost all seem to follow the same pattern.

First denial, the refusal to accept the mounting evidence that we are on the wrong track. Next, complacency: Even when the inconvenient facts are reluctantly acknowledged, a misplaced confidence that a small adjustment is all that is needed to snatch victory from the jaws of defeat. When that fails, the policy maker turns to wishful thinking, a doughty insistence on expecting the best in the face of the worst—everything will be all right; we have a plan premised on all the best possible assumptions. This is the terminal stage: At some point the full extent of the catastrophe is evident.

The inflation disaster unfolding in the U.S. is the latest proof that we learn nothing from our mistakes. We have clearly now reached the wishful-thinking phase of our leaders’ management of the crisis.

For almost a year we were told—by the president, the Treasury secretary and the Federal Reserve chairman, that unholy trinity of economic wisdom—that it wasn’t happening, or if it was, it was “transitory.” They soon progressed from denial to complacency. It will be fine, they insisted—it was all the fault of capitalist cupidity and rapacious Russians and could be dealt with accordingly.

Now, with consumer prices rising at the fastest rate in 40 years, the administration is deploying the power of positive thought: All will be fine—the Fed has got this. A few quick interest rate increases will squeeze the inflation out of the system, at minimal cost in growth and employment.

“My plan is to address inflation. It starts with a simple proposition: Respect the Fed and respect the Fed’s independence,” President Biden said a couple of weeks ago.

To be fair to Mr. Biden, Fed Chairman Jerome Powell apparently shares the dismiss-the-worst-and-hope-for-the-best strategy. He and his colleagues seem to believe that the gentlest of monetary squeezes will be enough to kill inflation without hurting the rest of the economy.

Among their March projections for key economic variables, the median forecast of members of the Fed’s monetary-policy-setting Open Market Committee, was that an increase in the federal-funds rate from the current 1% to just 2.8% would be sufficient to bring their favored measure of projected inflation down from 4.3% to 2.3% by 2024, with unemployment remaining at its current low and the economy continuing to grow.

That fantasy has already been cruelly exposed in less than three months, and the committee members are expected this week to inject a little economic reality into their forecasts when they raise rates again.

But whatever new realism they put on display this week is still likely to be filtered through a similar gauzy filter of wishfulness. The accumulating evidence from the depressing data is that the Fed’s challenge is much more severe than their optimism suggests.

One source of comfort for the wishful thinkers has been that the Fed won’t need to raise rates so aggressively in the current cycle because inflation is still well below the peak it reached in 1980, when Chairman Paul Volcker pushed interest rates to 20% to restrain price pressures.

But new research—published by the National Bureau of Economic Research and conducted by Harvard’s Larry Summers (a former Treasury secretary), Marijn Bolhuis of the International Monetary Fund and independent researcher Judd Cramer—suggests this may be, well, wishful thinking, backed by faulty comparisons.

Consumer-price inflation was measured in the early 1980s using a different basis for the cost of shelter. If today’s measure were used then, and given the weight it occupies in our current data, the inflation rate today would be much closer to what it was then. Official core CPI inflation (which doesn’t include food and energy) peaked in June 1980 at 13.6%, but measured by today’s standards, the number was 9.1%, the three economists estimate, a much smaller gap with today’s 6%. So the monetary squeeze required today may be much closer to the one Volcker produced then.

This adds a new dimension to the wishful-thinking phase of our current crisis. If a much more punishing set of rate hikes is needed now, do Mr. Powell and his colleagues have the stomach to do “whatever it takes” to get inflation down, as the current thinking has it?

Volcker endured exceptional pressure then, even from Ronald Reagan. Today’s political context is much less accommodating. The Fed has already been pressured to target social objectives in its monetary stance, such as minority unemployment rates. With elections looming and the Democrats already in a deep hole, will the Fed really have the fortitude to see through a monetary strategy that could send unemployment surging and the incumbent party swooning? Only a true wishful thinker could be confident of that.

![]() by drstrangelove » Thu Sep 29, 2022 10:54 pm

by drstrangelove » Thu Sep 29, 2022 10:54 pm

Pension Strategy Left Funds Vulnerable to Rate Increases

A pension-fund strategy that aims to reduce volatility without lowering returns created the first crack in the financial system after one of the fastest jumps in interest rates in decades.

The Bank of England stopped the selloff exacerbated by heavy selling from U.K. pension funds forced to raise cash.

The strategy is resulting in more modest selling in the U.S. as pension funds needed to increase collateral.

Pension funds adopted the so-called liability-driven investment strategy, or LDI, to address regulatory changes and help to close the gap between assets and liabilities. But the strategy faltered as interest rates surged and bond prices fell, forcing more selling and driving prices still lower.

“A vicious cycle kicks in and pension funds are selling and selling,” said Calum Mackenzie, an investment partner at pension-fund adviser Aon PLC. “What you start to see is a death spiral.”

These strategies largely took off after the global financial crisis, so these positions had never been tested in a period of rapidly rising interest rates, Mr. Mackenzie added.

The pension funds’ vulnerability stems from a strategy designed to cushion the impact of interest-rate movements.

The LDI strategy is meant to help pensions more efficiently manage their assets to ensure they can pay future retirees. Pensions use an LDI manager, who buys interest-rate swaps and other financial instruments to hedge against the risk that falling interest rates and rising inflation will increase their future obligations.

The LDI strategies also widely use leverage to try to close the gap between what they own and their future pension promises. “A LDI manager might buy £100 of interest rate exposure using £30 to £40 of the fund’s assets,” said Jon Hatchett, a partner at consulting firm Hymans Robertson.

That freed up assets to try to close pension-fund deficits but it increased the strain on the funds during the market turmoil, Mr. Hatchett said. “Those moves decimated the value of the assets backing the LDI portfolio,” he said.

The strategy was encouraged by U.K. regulators to help funds manage interest-rate risks. A guide from the pensions regulator said the strategy typically offers “an improved balance between investment risk and return but it does introduce additional risks.”

Some of the more than $1.8 trillion worth of corporate pension plans in the U.S. are also facing margin calls.

U.S. corporate pension plans managed by consulting firm and insurance brokerage Willis Towers Watson have posted tens of millions of dollars in collateral over the course of this year as bond prices have fallen, according to an estimate by portfolio manager John Delaney.

“It’s been a very interesting couple weeks, couple days,” said Mr. Delaney, whose firm manages $155 billion in global pension assets.

U.S. corporate pension plans have ramped up their use of derivatives over the past decade, analysts and pension managers said, after a 2006 federal requirement to measure their liabilities using long-term corporate bond rates.

While derivative-based LDI strategies have become more popular in the U.S., they are “nowhere near the scale used in the U.K.,” said Tom McCartan, a multisector portfolio manager who manages LDI strategies at Prudential Financial Inc.’s PGIM. U.S. pension plans can acquire 30-year corporate bonds and tap into Treasury STRIPS to accomplish goals that British plans seek to accomplish with derivatives, he said.

The Bank of England stopped the recent bond selloff caused in part by heavy selling from U.K. pension funds.

A pension-fund strategy that aims to reduce volatility without lowering returns created the first crack in the financial system after one of the fastest jumps in interest rates in decades.

The Bank of England stopped the selloff exacerbated by heavy selling from U.K. pension funds forced to raise cash.

The strategy is resulting in more modest selling in the U.S. as pension funds needed to increase collateral.

Pension funds adopted the so-called liability-driven investment strategy, or LDI, to address regulatory changes and help to close the gap between assets and liabilities. But the strategy faltered as interest rates surged and bond prices fell, forcing more selling and driving prices still lower.

Newsletter Sign-up

Markets

Major financial-market and trading news.

Subscribe

“A vicious cycle kicks in and pension funds are selling and selling,” said Calum Mackenzie, an investment partner at pension-fund adviser Aon PLC. “What you start to see is a death spiral.”

These strategies largely took off after the global financial crisis, so these positions had never been tested in a period of rapidly rising interest rates, Mr. Mackenzie added.

The pension funds’ vulnerability stems from a strategy designed to cushion the impact of interest-rate movements.

The LDI strategy is meant to help pensions more efficiently manage their assets to ensure they can pay future retirees. Pensions use an LDI manager, who buys interest-rate swaps and other financial instruments to hedge against the risk that falling interest rates and rising inflation will increase their future obligations.

The LDI strategies also widely use leverage to try to close the gap between what they own and their future pension promises. “A LDI manager might buy £100 of interest rate exposure using £30 to £40 of the fund’s assets,” said Jon Hatchett, a partner at consulting firm Hymans Robertson.

That freed up assets to try to close pension-fund deficits but it increased the strain on the funds during the market turmoil, Mr. Hatchett said. “Those moves decimated the value of the assets backing the LDI portfolio,” he said.

The strategy was encouraged by U.K. regulators to help funds manage interest-rate risks. A guide from the pensions regulator said the strategy typically offers “an improved balance between investment risk and return but it does introduce additional risks.”

‘A vicious cycle kicks in, and pension funds are selling and selling.’

— Calum Mackenzie, investment partner, Aon

Some of the more than $1.8 trillion worth of corporate pension plans in the U.S. are also facing margin calls.

U.S. corporate pension plans managed by consulting firm and insurance brokerage Willis Towers Watson have posted tens of millions of dollars in collateral over the course of this year as bond prices have fallen, according to an estimate by portfolio manager John Delaney.

“It’s been a very interesting couple weeks, couple days,” said Mr. Delaney, whose firm manages $155 billion in global pension assets.

U.S. corporate pension plans have ramped up their use of derivatives over the past decade, analysts and pension managers said, after a 2006 federal requirement to measure their liabilities using long-term corporate bond rates.

While derivative-based LDI strategies have become more popular in the U.S., they are “nowhere near the scale used in the U.K.,” said Tom McCartan, a multisector portfolio manager who manages LDI strategies at Prudential Financial Inc.’s PGIM. U.S. pension plans can acquire 30-year corporate bonds and tap into Treasury STRIPS to accomplish goals that British plans seek to accomplish with derivatives, he said.

Navigating the Stock Market

In the U.K., interest in LDI stems at least partly from British laws in the 1990s and mid 2000s that set funding requirements to try to better protect pensioners. Its use dates to at least the early 2000s, people in the LDI industry say.

Over the past decade, LDI has “become a core investment strategy for many pension schemes,” according to asset manager Schroders PLC. Pensions and others had invested £1.6 trillion in LDIs by 2021, up from £400 billion in 2011, data from trade group the Investment Association show.

The widespread adoption of LDI has been accompanied by higher levels of risk taking, according to the U.K. pensions regulator. Its 2019 survey of 137 big U.K. pension schemes found 45%, or almost half, had increased their use of leverage in the last five years. The maximum leverage allowed by the pensions ranged up to seven times, the survey found.

A spokesman said the pension regulator is now calling on trustees of company pensions and their advisers to “continue to review the resilience and liquidity of their investments, risk management and funding arrangements.”

This week’s bond meltdown is the first serious financial crisis to test how LDIs perform under extreme market conditions. The permeation of the strategy into pension plans affecting millions of people had largely gone unremarked. “The strategies have been below the radar,” said Peter Moizer, an accounting professor at the U.K.’s Leeds University Business School.

![]() by Belligerent Savant » Fri Nov 11, 2022 1:22 pm

by Belligerent Savant » Fri Nov 11, 2022 1:22 pm

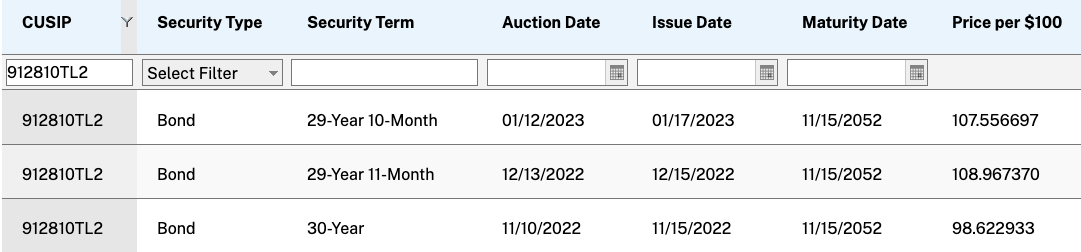

![]() by drstrangelove » Mon Feb 13, 2023 12:06 am

by drstrangelove » Mon Feb 13, 2023 12:06 am

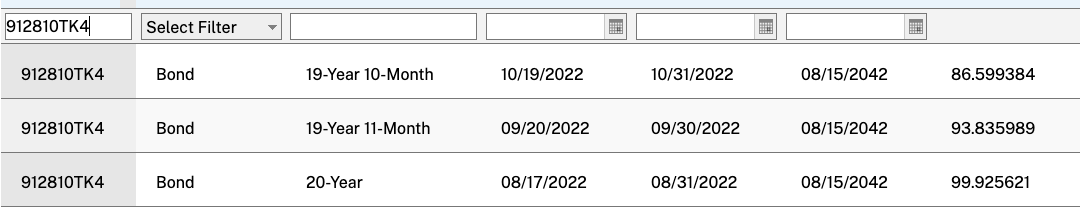

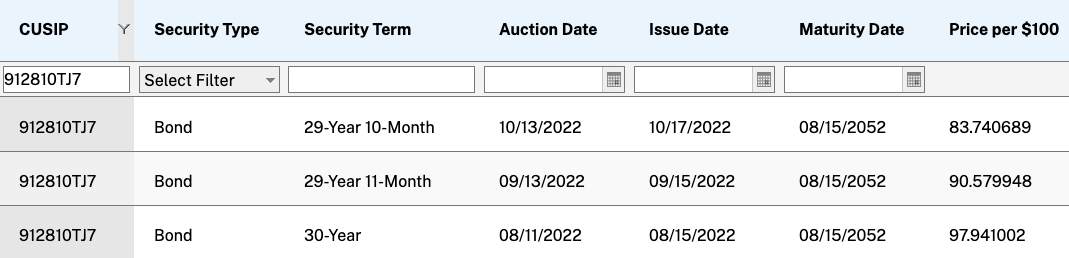

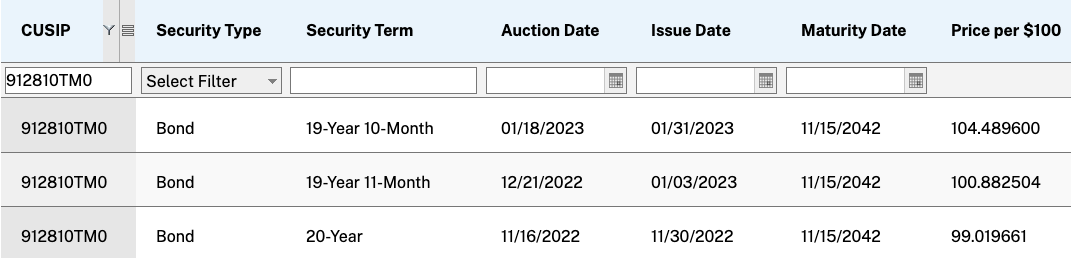

Market Collapse Due To Progressive Fires In The Bond Market

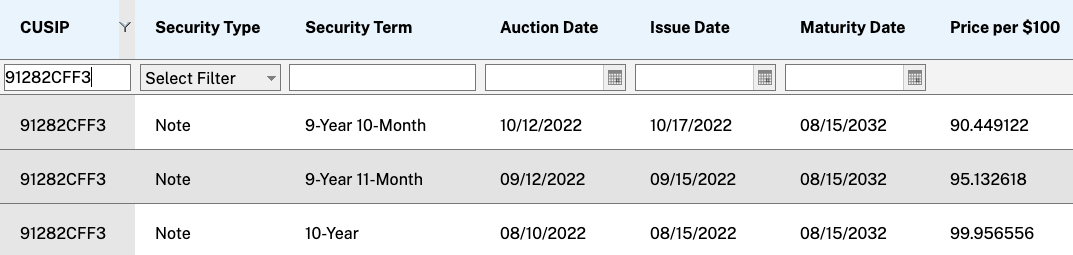

The US Fed started rate hikes February 1st 2022. Long-term US govt bonds auctions from this date start to take on higher and higher interest rates, which are fixed and due to be paid by the US govt every six months from the bonds issuance date for the bonds duration.

These are the price charts for US 10-year, 20-year, and 30-year bonds from that date.

Notice the massive price crashes leading into the start of February, May and November 2022. Followed by massive restorative price spikes in the middle of those months. These price spikes occur on the days of the 10Y, 20Y, and 30Y bond auctions held in February, May and November.

The higher the price of a bond at its date of auction, the lower the rate of interest assigned to it, which is fixed for its duration and paid every six months from its date of issuance.

Interest payments on the bonds from the February auction are due on the 15th of February and August each year.

Interest payments on the bonds from the May auction are due on the 15th of May and November each year.

Interest payments on the bonds from the November auction are due on the 15th of November and May each year.

Since the beginning of interest rate hikes in 2022 there have been three bear market rallies, which are brief periods of respite during stock market crashes in which stocks stop going down and start going up, before going back down again.

All three commenced about a month after the bonds auctions held in February, May, and November. The first two rallies, that of mid-late March and mid-June to mid-August, exactly one month after the bond auctions. The third rally, which we currently reside in as I write, that of late December to Mid-February, occurred a little over a month after.

And so we see a pattern. About a month after these bond auctions the stock market rallies to a point higher than it was on the auction date. But this was true only for those auctions preceded by a massive price crash before the auction date.

If someone had used the date of bond auctions alone without this specific qualifier as a buy signal, they would’ve got rinsed after the bond auctions in August where this wasn’t observed. Neither was it observed in the most recent auctions of February 2023.

In fact, the bond auctions in August marked the exact top of the largest bear market rally in 2022 and the beginning of the next leg down. And the same would appear to be true for the auctions of February 2023, putting an end to the current rally.

If this holds true we see a clear pattern. Massive price spike on bond auction date = bear market rally about a month later. No price spike on bond auction date = No rally and the next leg down.

This seems obvious enough. When bond prices crash the stock market follows. When bond prices stabilise the stock market follows. The price of bonds is the volume of music. When it dips below a certain level the music stops.

But why does the music play between the auctions of May and August. Then stop between the auctions of August and November. Then play gain between the auctions of November and February?

Each bond auction is followed by two months of “reissues”. Which are auctions of the same bonds with the same interest rates sold at whatever the new price is. So the bond auctions in May were reissue at auctions in June and July at the same rate of interest but new price.

And the price remains stables. Right up until the new auctions in August, after which the price begins to falls for the August reissues in September and October.

Then the price is restored for the November auctions and maintained, even increased, right through until the auctions in February.

The higher the price of bonds on the date of auction, the lower the interest rate. And this interest rate is due every six months from the date of issuance, which is always on the 15th of the month of auction.

Given that the price of bonds was much lower for the auctions in May and November than those in February and August, the increase of interest rates attached to bonds auctioned in May and November are much higher.

February 2022 Auctions

10Y 1.87%

20Y 2.37%

30Y 2.25%

May 2022 Auctions

10Y 2.87%

20Y 3.25%

30Y 2.87%

August 2022 Auctions

10Y 2.75%

20Y 3.37%

30Y 3%

November 2022 Auctions

10Y 4.12%

20Y 4%

30Y 4%

February 2023 Auctions

10Y 3.5%

20Y (Yet to Occur when written)

30Y 3.62%

Since these interest payments are due in every six months from the 15th of the month of auction, bonds auctioned in May and November have synchronised payments dates of May 15th and November 15th, while bonds auctioned in February and August have synchronised payment dates of February 15th and August 15th.

May & November 15th - payments on higher interest bonds due.

February & August 15th - payments on lower interest bonds due.

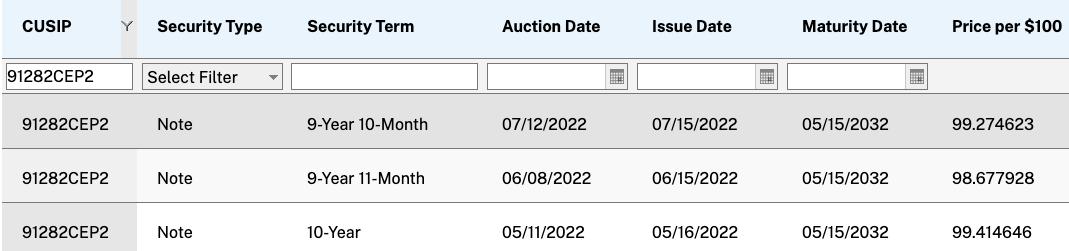

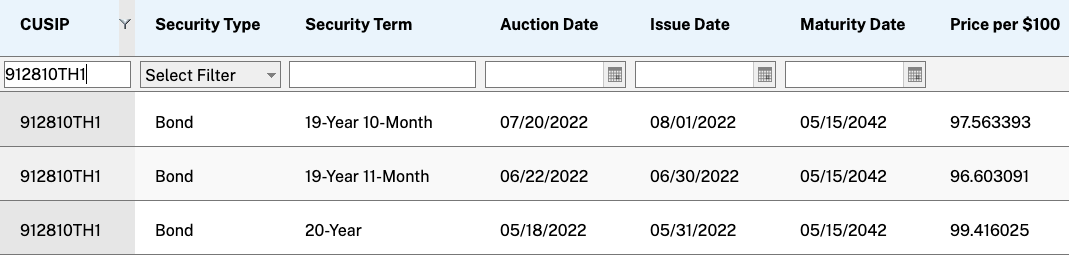

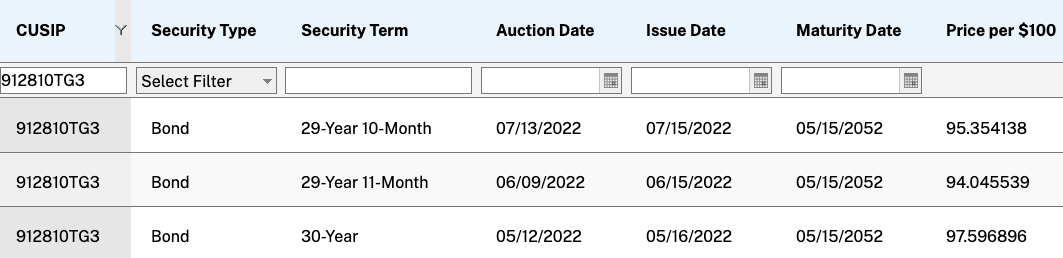

In the lead up to payments on the higher interest May/Nov bonds there are massive price crashes. Which means bondholders are selling.

^ May 10 year bond

^ May 20 year bond

^ May 30 year bond

What could cause the stock market to rally after the auction of May bonds, and then a crash in the price of May bonds just prior to the November auctions when interest on them is due?

Margin leverage followed by margin calls.

If bonds bought in May were used as collateral for margin loans, this could spark a rally in stocks. If this rally was then followed by a drop in the price of bonds, this could trigger margin calls and a forced selloff of all those bonds being used as collateral before the interest was due to be paid on them.

As it happens, pension funds all around the world have, for the past decade, been using a new financial mumbo jumbo conjured up in the wake of the global financial crisis. They call it Liability Driven Investment (LDI).

What Liability Driven Investment is’ is simple. A pension fund purchases a long term government bond. Then uses this bond as collateral to take out a cash loan they invest in stocks. This is just a margin loan. And it triggered a collapse in the price of UK bonds in September 2022. The value of long term Uk government bonds fell below a price which forced pension funds using them as collateral to sell them, which forced the price down even further forcing more pension funds to sell them in a sort of death spiral.

Much was made of this event though little attention was paid to what had actually happened. As you can see from the charts the price of UK bonds started crashing around the middle of August, a month before Truss announced her budget in September, which was just a cherry on the cake.

What actually happened is the central bank graciously repurchased bonds they’d auctioned to pension funds forced to sell them at decades low. The central bank then resold these for a profit a few months later.

"Practically laughing at the pivot folks, the Bank of England announced today that it sold the entire £19.3 billion in UK government bonds — £12.1 billion of long-dated conventional gilts and £7.2 billion in inflation-protected gilts – that it had purchased between September 28 and October 14 during the UK pension fund crisis that had threatened to send contagion in all directions. And it sold the gilts for £23.1 billion, making a profit of £3.8 billion, or 19.7% in about three months!" - https://wolfstreet.com/2023/01/12/bank- ... -outright/

This wasn’t an isolated event. It happened in the Netherlands as well earlier last year.

"Last year, the Netherlands saw a drama which might seem familiar to UK investors. Within the first six months of 2022, Dutch pension funds sold €88bn (£77.1bn) in assets, this amounts to nearly 5% of their total assets, according to Dutch central bank DNB. Assets managed by Dutch pension funds dropped to €1.4trn (£1,2trn), from €1.8trn (£1.5trn) last year.

The reason for these outflows is the growing costs of collateral calls on DB scheme’s derivative positions. Amid rising interest rates, these derivatives turned out to be an expensive hedge to hold. The resemblance between the Dutch and British LDI crisis is uncanny." - https://www.portfolio-institutional.co. ... therlands/

BlackRock was the primary provider of LDI service to the UK pension funds which had received margin calls, and they provide these same LDI services to US corporate pension funds.

In August 2019 BlackRock published a white paper proposal to become a bond purchasing agent for the US Fed. This proposal was accepted a few months as part of the emergency measures in response to the pandemic.

Larry Fink’s protege Wally Adeyemo operates inside the Treasury as deputy secretary. All the mechanisms and levers are there for a controlled demolition. Music on. Music off. Music on. Music off. If this theory holds the following will happen.

In a few days on February 15th the price of the 20 year bond will crash more than -5%. Bond prices will continue to crash until early May and the US stock market will follow and crash to new lows. Then in May, if we see a restorative spike in the price of bonds during the auctions in May, expect another bear market rally until August. If not, then down into the abyss.

![]() by drstrangelove » Mon Feb 13, 2023 5:20 am

by drstrangelove » Mon Feb 13, 2023 5:20 am

![]() by drstrangelove » Mon Feb 20, 2023 11:26 am

by drstrangelove » Mon Feb 20, 2023 11:26 am

![]() by Belligerent Savant » Mon Feb 20, 2023 11:39 am

by Belligerent Savant » Mon Feb 20, 2023 11:39 am

Users browsing this forum: No registered users and 6 guests

Powered by phpBB® Forum Software © phpBB Group

Site design by Likely Arts based on "Deluxe" by Artodia.