JackRiddler wrote:The resources are already there, you just have to be ready to give up the annual 57 pounds of beef per capita.

I must say, in the last year I'm buying/eating much less beef. I'd like to see more goats and goat products.

Moderators: Elvis, DrVolin, Jeff

![]() by Elvis » Wed Jan 27, 2021 11:37 am

by Elvis » Wed Jan 27, 2021 11:37 am

JackRiddler wrote:The resources are already there, you just have to be ready to give up the annual 57 pounds of beef per capita.

![]() by Elvis » Fri Feb 05, 2021 3:00 pm

by Elvis » Fri Feb 05, 2021 3:00 pm

https://realprogressives.org/podcast_ep ... ohan-grey/

Digitizing the Dollar: The Battle for the Soul of Public Money in the Age of Cryptocurrency

https://www.youtube.com/watch?v=PlkRxCYgx3A

In March, Rohan Grey was the guest speaker on a Real Progressives National Outreach Call. He talked about his forthcoming book, Digitizing the Dollar: The Battle for the Soul of Public Money in the Age of Cryptocurrency. The title says it all.

In the midst of the pandemic, people are living with unprecedented financial insecurity. There’s no real sense of when they’ll be able to return to work or whether there will be jobs awaiting them. Rohan had been working with Representative Rashida Tlaib on her emergency assistance act, which is designed to provide relief funds of $2,000 a month to every man, woman, and child in the US. He explained the thinking that went into drawing up the bill, which is far more generous than any other coronavirus stimulus bill to this day.

Of special interest to proponents of MMT is the fact that the Treasury would finance the program through minting trillion-dollar coins. Rohan told us how this provides a legal workaround to arguments about the debt-ceiling.

The distribution method is also of interest to MMT-ers and it leads to the central topic of the presentation: digital currency. A debit card would be issued to everyone, sent by mail or available for pickup at numerous distribution centers. The debit cards themselves are to be privacy-protected. That issue – privacy – must be at the heart of any plans for cryptocurrency.

The goal in designing the bill was that it be as simple, universal, and accessible as possible, but there’s nothing simple about the reasoning and planning that went into it. Rohan walks us through the process, showing the logic behind each choice.

Fans of this podcast are familiar with Rohan Grey’s ability to explain complicated issues in a clear and fascinating way, making connections between ideas and facts, contemporary and historical. He refers to ancient Mesopotamian temples and Seinfeld plots to make a point. He is the ideal teacher to guide us through the maze of technical and moral issues we confront when dealing with digital currency.

When asked about the phrase from the title of his book – the battle for the soul of public money – Rohan says that this is the soul of the human race. It’s the soul of democracy. We put our hopes and dreams, our personalities, and our experiences into our computers every time we use Google or Facebook. More to the point here, every time we use Venmo or Paypal. The net that holds those souls either respects our freedom and privacy or it doesn’t. It’s either a tool of emancipation that connects us as equals or it’s a tool of control and subjugation. Do we entrust it to private corporations?

In the battle for the soul of public money, “it’s hard enough to learn about money — and about law. Now we’re adding technology. Those three worlds are converging at a rapid pace. The fight we’re facing is for a just money system, and when we get that money, it isn’t a snitch, isn’t a traitor.”

In discovering why we need to struggle for the soul of public money, this episode takes us straight to the heart of the matter.

Rohan Grey is the founder and president of the Modern Money Network, a research scholar at the Global Institute for Sustainable Prosperity, and a J.S.D. candidate at Cornell Law School, where his research focuses on the law of money in the internet society.

![]() by BenDhyan » Mon Feb 08, 2021 7:42 pm

by BenDhyan » Mon Feb 08, 2021 7:42 pm

It Doesn't Get More Buzzy Than This: Tesla Is Investing $1.5 Billion In Bitcoin

February 8, 2021

Electric automaker Tesla and cryptocurrency Bitcoin have a lot in common.

Both have seen their market value skyrocket last year, defying skeptics and thrilling fans. Both are fueled by mass enthusiasm and techno-utopian idealism.

And they've both got plenty of doubters warning a giant crash could be on the horizon.

So when Tesla announced it would purchase $1.5 billion worth of bitcoin on Monday, and that it would accept the currency from customers in the future, it might have been tempting to dismiss this as an outlier — an oddball move from a company run by an eccentric CEO.

But Tesla is not the only mainstream company starting to take Bitcoin seriously. Asset manager BlackRock, life insurance giant MassMutual and payment companies Square and Paypal have all dipped their toes in the Bitcoin waters.

Meanwhile, enterprise software company MicroStrategy did more of a cannonball. The company's CEO, Michael Saylor, describes himself as a bitcoin evangelist. Last year he took pretty much all of the company's cash and put it into Bitcoin. Then he borrowed even more money and put that into Bitcoin, too.

"People that didn't like Bitcoin, they thought we were crazy," he says. "But the people that like Bitcoin thought that was brilliant, and the shareholders liked it."

That's an understatement. MicroStrategy's stock has skyrocketed right alongside Bitcoin values.

https://www.npr.org/2021/02/08/965494932/it-doesnt-get-more-buzzy-than-this-tesla-is-investing-1-5-billion-in-bitcoin

![]() by Belligerent Savant » Tue Feb 09, 2021 3:09 pm

by Belligerent Savant » Tue Feb 09, 2021 3:09 pm

Is Bitcoin A Ponzi Scheme? Point By Point Analysis

Feb. 09, 2021 9:30 AM ETBitcoin USD (BTC-USD)GBTCGLDXLF148 Comments57 Likes

Summary

- Bitcoin is sometimes called a Ponzi scheme, so this article compared the Bitcoin protocol to an official list of Ponzi characteristics to see if it holds up.

- Bitcoin does not meet most of the criteria for a Ponzi scheme.

- However, an investor must assess the ongoing probability of Bitcoin failing or succeeding in displacing other stores of value and payment systems.

One of the concerns I’ve seen aimed at Bitcoin is the claim that it’s a Ponzi scheme. The argument suggests that because the Bitcoin network is continually reliant on new people buying in, that eventually it will collapse in price as new buyers are exhausted.

So, this article takes a serious look at the concern by comparing and contrasting Bitcoin to systems that have Ponzi-like characteristics, to see if the claim holds up.

The short answer is that Bitcoin does not meet the definition of a Ponzi scheme in either narrow or broad sense, but let’s dive in to see why that’s the case.

Defining a Ponzi Scheme

To start with tackling the topic of Bitcoin as a Ponzi scheme, we need a definition.

Here is how the US Securities and Exchange Commission defines one:

A Ponzi scheme is an investment fraud that pays existing investors with funds collected from new investors. Ponzi scheme organizers often promise to invest your money and generate high returns with little or no risk. But in many Ponzi schemes, the fraudsters do not invest the money. Instead, they use it to pay those who invested earlier and may keep some for themselves.

With little or no legitimate earnings, Ponzi schemes require a constant flow of new money to survive. When it becomes hard to recruit new investors, or when large numbers of existing investors cash out, these schemes tend to collapse.

Ponzi schemes are named after Charles Ponzi, who duped investors in the 1920s with a postage stamp speculation scheme.

They further go on to list red flags to look out for:

Many Ponzi schemes share common characteristics. Look for these warning signs:

High returns with little or no risk. Every investment carries some degree of risk, and investments yielding higher returns typically involve more risk. Be highly suspicious of any “guaranteed” investment opportunity.

Overly consistent returns. Investments tend to go up and down over time. Be skeptical about an investment that regularly generates positive returns regardless of overall market conditions.

Unregistered investments. Ponzi schemes typically involve investments that are not registered with the SEC or with state regulators. Registration is important because it provides investors with access to information about the company’s management, products, services, and finances.

Unlicensed sellers. Federal and state securities laws require investment professionals and firms to be licensed or registered. Most Ponzi schemes involve unlicensed individuals or unregistered firms.

Secretive, complex strategies. Avoid investments if you don’t understand them or can’t get complete information about them.

Issues with paperwork. Account statement errors may be a sign that funds are not being invested as promised.

Difficulty receiving payments. Be suspicious if you don’t receive a payment or have difficulty cashing out. Ponzi scheme promoters sometimes try to prevent participants from cashing out by offering even higher returns for staying put.

I think that’s a great set of information to work with. We can see how many of those attributes, if any, Bitcoin has.

Bitcoin’s Launch Process

Before we get into comparing Bitcoin point-by-point to the above list, we can start with a recap of how Bitcoin was launched.

In August 2008, someone identifying himself as Satoshi Nakamoto created Bitcoin.org.

Two months later in October 2008, Satoshi released the Bitcoin white paper. This document explained how the technology would work, including the solution to the double-spending problem. As you can see from the link, it was written in the format and style of an academic research paper, since it was presenting a major technical breakthrough that provided a solution for well-known computer science challenges related to digital scarcity. It contained no promises of enrichment or returns.

Then, three months later in January 2009, Satoshi published the initial Bitcoin software. In the custom genesis block of the blockchain, which contains no spendable Bitcoin, he provided a time-stamped article headline about bank bailouts from The Times of London, likely to prove that there was no pre-mining and to set the tone for the project. From there, it took him six days to finish things and mine block 1, which contained the first 50 spendable bitcoins, and he released the Bitcoin source code that day on January 9th. By January 10th, Hal Finney publicly tweeted that he was running the Bitcoin software as well, and right from the beginning, Satoshi was testing the system by sending bitcoins to Hal.

Interestingly, since Satoshi showed how to do it with the white paper more than two months before launching the open source Bitcoin software himself, technically someone could have used the newfound knowledge to launch a version before him. It would have been unlikely, due to Satoshi’s big head start in figuring all of this out and understanding it at a deep level, but it was technically possible. He gave away the key technological breakthrough before he launched the first version of the project. Between the publication of the white paper and the launch of the software, he answered questions and explained his choices for his white paper to several other cryptographers on an email list in response to their critiques, almost like an academic thesis defense, and several of them could have been technical enough to “steal” the project from him, if they were less skeptical.

After launch, a set of equipment that is widely believed to belong to Satoshi remained a large Bitcoin miner throughout the first year. Mining is necessary to keep verifying transactions for the network, and bitcoins had no quoted dollar price at that time. He gradually reduced his mining over time, as mining became more distributed across the network. There are nearly 1 million bitcoins that are believed to belong to Satoshi that he mined through Bitcoin’s early period and that he has never moved from their initial address. He could have cashed out at any point with billions of dollars in profit, but so far has not, over a decade into the project’s life. It’s not known if he is still alive, but other than some early coins for test transactions, the bulk of his coins haven’t moved.

Not long after, he transferred ownership of his website domains to others, and ever since, Bitcoin has been self-sustaining among a revolving development community with no input from Satoshi.

Bitcoin is open source, and is distributed around the world. The blockchain is public, transparent, verifiable, auditable, and analyzable. Firms can do analytics of the entire blockchain and see which bitcoins are moving or remaining in place in various addresses. An open source full node can be run on a basic home computer, and can audit Bitcoin’s entire money supply and other metrics.

With that in mind, we can then compare Bitcoin to the red flags of being a Ponzi scheme.

Investment Returns: Not Promised

Satoshi never promised any investment returns, let alone high investment returns or consistent investment returns. In fact, Bitcoin was known for the first decade of its existence as being extremely high-volatility speculation. For the first year and a half, Bitcoin had no quotable price, and after that, it had a very volatile price.

The online writings from Satoshi still exist, and he barely ever talked about financial gain. He mostly wrote about technical aspects, about freedom, about the problems of the modern banking system, and so forth. Satoshi wrote mostly like a programmer, occasionally like an economist, and never like a salesman.

We have to search pretty deeply to find instances where he discussed Bitcoin potentially becoming valuable. When he did talk about the potential value or price of a Bitcoin, he spoke very matter-of-factly in regards to how to categorize it, whether it would be inflationary or deflationary, and admitted a ton of variance for how the project could turn out. Digging around for Satoshi’s quotes on the price of value of a Bitcoin, here’s what I found:

The fact that new coins are produced means the money supply increases by a planned amount, but this does not necessarily result in inflation. If the supply of money increases at the same rate that the number of people using it increases, prices remain stable. If it does not increase as fast as demand, there will be deflation and early holders of money will see its value increase.

___

It might make sense just to get some in case it catches on. If enough people think the same way, that becomes a self-fulfilling prophecy. Once it gets bootstrapped, there are so many applications if you could effortlessly pay a few cents to a website as easily as dropping coins in a vending machine.

___

In this sense, it’s more typical of a precious metal. Instead of the supply changing to keep the value the same, the supply is predetermined and the value changes. As the number of users grows, the value per coin increases. It has the potential for a positive feedback loop; as users increase, the value goes up, which could attract more users to take advantage of the increasing value.

___

Maybe it could get an initial value circularly as you’ve suggested, by people foreseeing its potential usefulness for exchange. (I would definitely want some) Maybe collectors, any random reason could spark it. I think the traditional qualifications for money were written with the assumption that there are so many competing objects in the world that are scarce, an object with the automatic bootstrap of intrinsic value will surely win out over those without intrinsic value. But if there were nothing in the world with intrinsic value that could be used as money, only scarce but no intrinsic value, I think people would still take up something. (I’m using the word scarce here to only mean limited potential supply).

___

A rational market price for something that is expected to increase in value will already reflect the present value of the expected future increases. In your head, you do a probability estimate balancing the odds that it keeps increasing.

___

I’m sure that in 20 years there will either be very large transaction volume or no volume.

___

Bitcoins have no dividend or potential future dividend, therefore not like a stock. More like a collectible or commodity.

–Quotes by Satoshi Nakamoto

Promising unusually high or consistent investment returns is a common red flag for being a Ponzi scheme, and with Satoshi’s original Bitcoin, there was none of that.

Over time, Bitcoin investors have often predicted very high prices (and so far those predictions have been correct), but the project itself from inception did not have those attributes.

Open Source: The Opposite of Secrecy

Most Ponzi schemes rely on secrecy. If the investors understood that an investment they owned was actually a Ponzi scheme, they would try to pull their money out immediately. This secrecy prevents the market from appropriately pricing the investment until the secret gets found out.

For example, investors in Bernie Madoff’s scheme thought they owned a variety of assets. In reality, earlier investor outflows were just being paid back from new investor inflows, rather than money being made from actual investments. The investments listed on their statements were fake, and for any of those clients, it would be nearly impossible to verify that they are fake.

Bitcoin, however, works on precisely the opposite set of principles. As a distributed piece of open source software that requires majority consensus to change, every line of code is known, and no central authority can change it. A key tenet of Bitcoin is to verify rather than to trust. Software to run a full node can be freely downloaded and run on a normal PC, and can audit the entire blockchain and the entire money supply. It relies on no website, no critical data center, and no corporate structure.

For this reason, there are no “issues with paperwork” or “difficulty receiving payments”, referencing some of the SEC red flags of a Ponzi. The entire point of Bitcoin is to not rely on any third parties; it is immutable and self-verifiable. Bitcoin can only be moved with the private key associated with a certain address, and if you use your private key to move your bitcoins, there is nobody who can stop you from doing so.

There are of course some bad actors in the surrounding ecosystem. People relying on others to hold their private keys (rather than doing so themselves) have sometimes lost their coins due to bad custodians, but not because the core Bitcoin software failed. Third-party exchanges can be fraudulent or can be hacked. Phishing schemes or other frauds can trick people into revealing their private keys or account information. But these are not associated with Bitcoin itself, and as people use Bitcoin, they must ensure they understand how the system works to avoid falling for scams in the ecosystem.

Bitcoin vs Gold Market

Some people assert that Bitcoin is a Ponzi scheme because it relies on an ever-larger pool of investors coming into the space to buy from earlier investors.

To some extent this reliance on new investors is correct; Bitcoin keeps growing its network effect, reaching more people and bigger pools of money, which keeps increasing its usefulness and value.

Bitcoin will only be successful in the long run if its market capitalization reaches and sustains a very high level, in part because its security (hash rate) is inherently connected to its price. If for some reason demand for it were to permanently flatline and turn down without reaching a high enough level, Bitcoin would remain a niche asset and its value, security, and network effect could deteriorate over time. This could begin a vicious cycle of attracting fewer developers to keep building out its secondary layers and surrounding hardware/software ecosystem, potentially resulting in quality stagnation, price stagnation, and security stagnation.

However, this doesn’t make it a Ponzi scheme, because, by similar logic, gold is a 5,000 year old Ponzi scheme. The vast majority of gold’s usage is not for industry; it’s for storing and displaying wealth. It produces no cash flows, and is only worth what someone else will pay for it. If peoples’ jewelry tastes change, and if people no longer view gold as an optimal store of value, its network effect could diminish.

There are 60+ years of gold’s annual production supply estimated to be available in various forms around the world. And that’s more like 500 years worth of industrial-only supply, factoring out jewelry and store-of-value demand. Therefore, gold’s supply/demand balance to support a high price requires the ongoing perception of gold as an attractive way to store and display wealth, which is somewhat subjective. Based on the industrial-only demand, there is a ton of excess supply and prices would be way lower.

However, gold’s monetary network effect has remained robust for such a long period of time because the collection of unique properties it has is what made it continually regarded as being optimal for long-term wealth preservation and jewelry across generations: it’s scarce, pretty, malleable, fungible, divisible, and nearly chemically indestructible. As fiat currencies around the world come and go, and rapidly increase their per-unit number, gold’s supply remains relatively scarce, only growing by about 1.5% per year. According to industry estimates, there is about one ounce of above-ground gold per person in the world.

Similarly, Bitcoin relies on the network effect, meaning a sufficiently large number of people need to view it as a good holding for it to retain its value. But a network effect is not a Ponzi scheme in and of itself. Prospective investors can analyze the metrics of Bitcoin’s network effect, and determine for themselves the risk/reward of buying into it.

Bitcoin vs Fiat Banking System

By the broadest definition of a Ponzi scheme, the entire global banking system is a Ponzi scheme.

Firstly, fiat currency is an artificial commodity, in a certain sense. A dollar, in and of itself, is just an object made out of paper, or represented on a digital bank ledger. Same for the euro, the yen, and other currencies. It pays no cash flows on its own, although institutions that hold it for you might be willing to pay you a yield (or, in some cases, could charge you a negative yield). When we do work or sell something to acquire dollars, we do so only with the belief that its large network effect (including a legal/government network effect) will ensure that we can take these pieces of paper and give them to someone else for something of value.

Secondly, when we organize these pieces of paper and their digital representations in a fractional-reserve banking system, we add another complicated layer. If about 20% of people were to try to pull their money out of their bank at the same time, the banking system would collapse. Or more realistically, the banks would just say “no” to your withdrawal, because they don’t have the cash. This happened to some US banks in early 2020 during the pandemic shutdown, and occurs regularly around the world. That’s actually one of the SEC’s red flags of a Ponzi scheme: difficulty receiving payments.

In the well-known musical chairs game, there is a set of chairs, someone plays music, and kids (of which there is one more than the number of chairs) start walking in circles around the chairs. When the music stops, all of the kids scramble to sit in one of the chairs. One slow or unlucky kid doesn’t get a seat, and therefore leaves the game. In the next round, one chair is removed, and the music resumes for the remaining kids. Eventually, after many rounds, there are two kids and one seat, and then there is a winner when that round ends.

The banking system is a permanent round of musical chairs. There are more kids than chairs, so they can’t all get one. If the music were to stop, this would become clear. However, as long as the music keeps going (with occasional bailouts via printed money), it keeps moving along.

Banks collect depositor cash, and use their capital to make loans and buy securities. Only a small fraction of depositor cash is available for withdrawal. A bank’s assets consist of loans owed to them, securities such as Treasuries, and cash reserves. Their liabilities consist of money owed to depositors, as well as any other liabilities they may have like bonds issued to creditors.

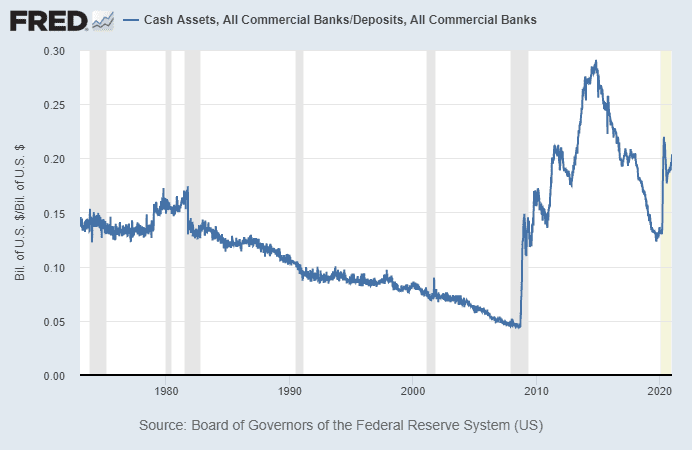

For the United States, banks collectively have about 20% of customer deposits held as cash reserves:

Chart Source: St. Louis Fed

As the chart shows, this percentage reached below 5% prior to the global financial crisis (which is why the crisis was so bad, and marked the turning point in the long-term debt cycle), but with quantitative easing, new regulations, and more self-regulation, banks now have about 20% of deposit balances as reserves.

Similarly, the total amount of physical cash in circulation, which is exclusively printed by the US Treasury Department, is only about 13% as much as the amount of commercial bank deposits, and only a tiny fraction of that is actually held by banks as vault cash. There’s not nearly enough physical cash (by design), for a significant percentage of people to pull their capital out of banks at once. People run into “difficulty receiving payments” if enough of them do so around the same time.

As constructed in the current way, the banking system can never end. If a sufficiently large number of banks were to liquidate, the entire system would cease to function.

If a single bank were to liquidate without being acquired, it would hypothetically have to sell all of its loans and securities to other banks, convert it all to cash, and pay that cash out to depositors. However, if a sufficiently large number of banks were to do that at once, the market value of the assets they are selling would sharply decrease and the market would turn illiquid, because there are not enough available buyers.

Realistically, if enough banks were to liquidate at once, and the market froze up as debt/loan sellers overwhelmed buyers, the Federal Reserve would end up creating new dollars to buy assets to re-liquidity the market, which would radically increase the number of dollars in circulation. Otherwise, everything nominally collapses, because there aren’t enough currency units in the system to support an unwinding of the banking systems’ assets.

So, the monetary system functions as a permanent round of musical chairs on top of artificial government-issued commodities, where there are by far more claims on that money (the kids) than money that is currently available to them (the chairs) if they were to all scramble for it at once. The number of kids and chairs both keeps growing, but there are always way more kids than chairs. Whenever the system partially breaks, a couple more chairs are added to the round to keep it going.

We accept this as normal, because we assume it will never end. The fractional reserve banking system has functioned around the world for hundreds of years (first gold-backed, and then totally fiat-based), albeit with occasional inflationary events along the way to partially reset things.

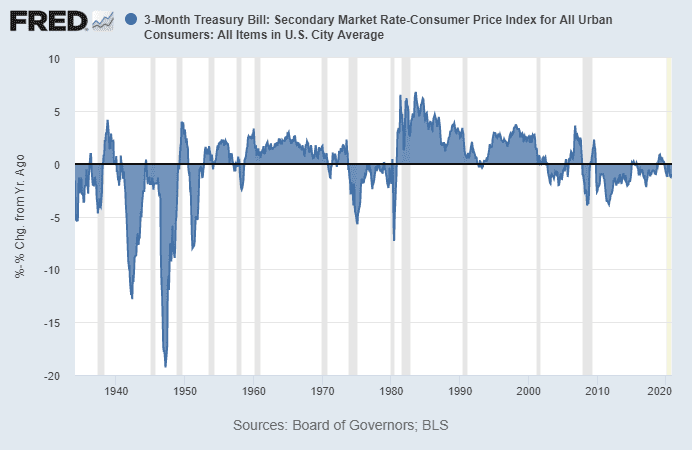

Each individual unit of fiat currency has degraded about 99% in value or more over the multi-decade timeline. This means that investors either need to earn a rate of interest that exceeds the real inflation rate (which is not currently happening), or they need to buy investments instead, which inflates the value of stocks and real estate compared to their cash flows, and pushes up the prices of scarce objects like fine art.

Over the past century, T-bills and bank cash just kept up with inflation, providing no real return. However, this tends to be very lumpy. There were decades such as the 1940s, 1970s, and 2010s, where holders of T-bills and bank cash persistently failed to keep up with inflation. This chart shows the T-bill rate minus the official inflation rate over nine decades:

Chart Source: St. Louis Fed

Bitcoin is an emergent deflationary savings and payments technology that is mostly used in an unlevered way, meaning that most people just buy it, hold it, and occasionally trade it. There are some Bitcoin banks, and some folks that use leverage on exchanges, but overall debt in the system remains low relative to market value, and you can self-custody your own holdings.

![]() by Elvis » Wed Feb 10, 2021 8:01 am

by Elvis » Wed Feb 10, 2021 8:01 am

Feb. 09, 2021 9:30 AM ETBitcoin USD (BTC-USD)GBTCGLDXLF148 wrote:

in a fractional-reserve banking system [...] If about 20% of people were to try to pull their money out of their bank at the same time, the banking system would collapse. Or more realistically, the banks would just say “no” to your withdrawal, because they don’t have the cash.

[...]

Banks collect depositor cash, and use their capital to make loans and buy securities.

if enough banks were to liquidate at once, and the market froze up as debt/loan sellers overwhelmed buyers, the Federal Reserve would end up creating new dollars to buy assets to re-liquidity the market, which would radically increase the number of dollars in circulation.

![]() by Belligerent Savant » Wed Feb 10, 2021 9:33 am

by Belligerent Savant » Wed Feb 10, 2021 9:33 am

Relative to any other asset class or portfolio hedge, cryptocurrencies would uniquely protect portfolios against a simultaneous loss of faith in a country’s currency and its payments system, because they are produced and they circulate outside conventional and regulated channels.

...

...as insurance (or a lottery ticket) against dystopia, some exposure to these assets could be always justified irrespective of liquidity and volatility concerns

![]() by dada » Wed Feb 10, 2021 10:35 am

by dada » Wed Feb 10, 2021 10:35 am

![]() by Belligerent Savant » Wed Feb 10, 2021 12:40 pm

by Belligerent Savant » Wed Feb 10, 2021 12:40 pm

![]() by dada » Wed Feb 10, 2021 4:01 pm

by dada » Wed Feb 10, 2021 4:01 pm

![]() by dada » Wed Feb 10, 2021 4:43 pm

by dada » Wed Feb 10, 2021 4:43 pm

![]() by Belligerent Savant » Wed Feb 10, 2021 7:17 pm

by Belligerent Savant » Wed Feb 10, 2021 7:17 pm

Saying that the total digitization of cash would not be a deterrent to illegal trade. People will find a way. A perfectly trackable cash won't suppress addictions and dark desires, to believe that would be to misunderstand some of the most basic drivers of society.

![]() by dada » Wed Feb 10, 2021 8:26 pm

by dada » Wed Feb 10, 2021 8:26 pm

![]() by Elvis » Wed Feb 10, 2021 8:30 pm

by Elvis » Wed Feb 10, 2021 8:30 pm

Elvis » Fri Feb 05, 2021 12:00 pm wrote:https://realprogressives.org/podcast_ep ... ohan-grey/

Digitizing the Dollar: The Battle for the Soul of Public Money in the Age of Cryptocurrency

https://www.youtube.com/watch?v=PlkRxCYgx3A

In March, Rohan Grey was the guest speaker on a Real Progressives National Outreach Call. He talked about his forthcoming book, Digitizing the Dollar: The Battle for the Soul of Public Money in the Age of Cryptocurrency. The title says it all.

In the midst of the pandemic, people are living with unprecedented financial insecurity. There’s no real sense of when they’ll be able to return to work or whether there will be jobs awaiting them. Rohan had been working with Representative Rashida Tlaib on her emergency assistance act, which is designed to provide relief funds of $2,000 a month to every man, woman, and child in the US. He explained the thinking that went into drawing up the bill, which is far more generous than any other coronavirus stimulus bill to this day.

Of special interest to proponents of MMT is the fact that the Treasury would finance the program through minting trillion-dollar coins. Rohan told us how this provides a legal workaround to arguments about the debt-ceiling.

The distribution method is also of interest to MMT-ers and it leads to the central topic of the presentation: digital currency. A debit card would be issued to everyone, sent by mail or available for pickup at numerous distribution centers. The debit cards themselves are to be privacy-protected. That issue – privacy – must be at the heart of any plans for cryptocurrency.

The goal in designing the bill was that it be as simple, universal, and accessible as possible, but there’s nothing simple about the reasoning and planning that went into it. Rohan walks us through the process, showing the logic behind each choice.

Fans of this podcast are familiar with Rohan Grey’s ability to explain complicated issues in a clear and fascinating way, making connections between ideas and facts, contemporary and historical. He refers to ancient Mesopotamian temples and Seinfeld plots to make a point. He is the ideal teacher to guide us through the maze of technical and moral issues we confront when dealing with digital currency.

When asked about the phrase from the title of his book – the battle for the soul of public money – Rohan says that this is the soul of the human race. It’s the soul of democracy. We put our hopes and dreams, our personalities, and our experiences into our computers every time we use Google or Facebook. More to the point here, every time we use Venmo or Paypal. The net that holds those souls either respects our freedom and privacy or it doesn’t. It’s either a tool of emancipation that connects us as equals or it’s a tool of control and subjugation. Do we entrust it to private corporations?

In the battle for the soul of public money, “it’s hard enough to learn about money — and about law. Now we’re adding technology. Those three worlds are converging at a rapid pace. The fight we’re facing is for a just money system, and when we get that money, it isn’t a snitch, isn’t a traitor.”

In discovering why we need to struggle for the soul of public money, this episode takes us straight to the heart of the matter.

Rohan Grey is the founder and president of the Modern Money Network, a research scholar at the Global Institute for Sustainable Prosperity, and a J.S.D. candidate at Cornell Law School, where his research focuses on the law of money in the internet society.

![]() by Belligerent Savant » Wed Feb 10, 2021 8:46 pm

by Belligerent Savant » Wed Feb 10, 2021 8:46 pm

dada » Wed Feb 10, 2021 7:26 pm wrote:Not really. Just thinking freely here.

![]() by Elvis » Wed Feb 10, 2021 8:54 pm

by Elvis » Wed Feb 10, 2021 8:54 pm

Users browsing this forum: No registered users and 8 guests

Powered by phpBB® Forum Software © phpBB Group

Site design by Likely Arts based on "Deluxe" by Artodia.